CSMP IAS : India's Premier Coaching Institute for IAS / PCS

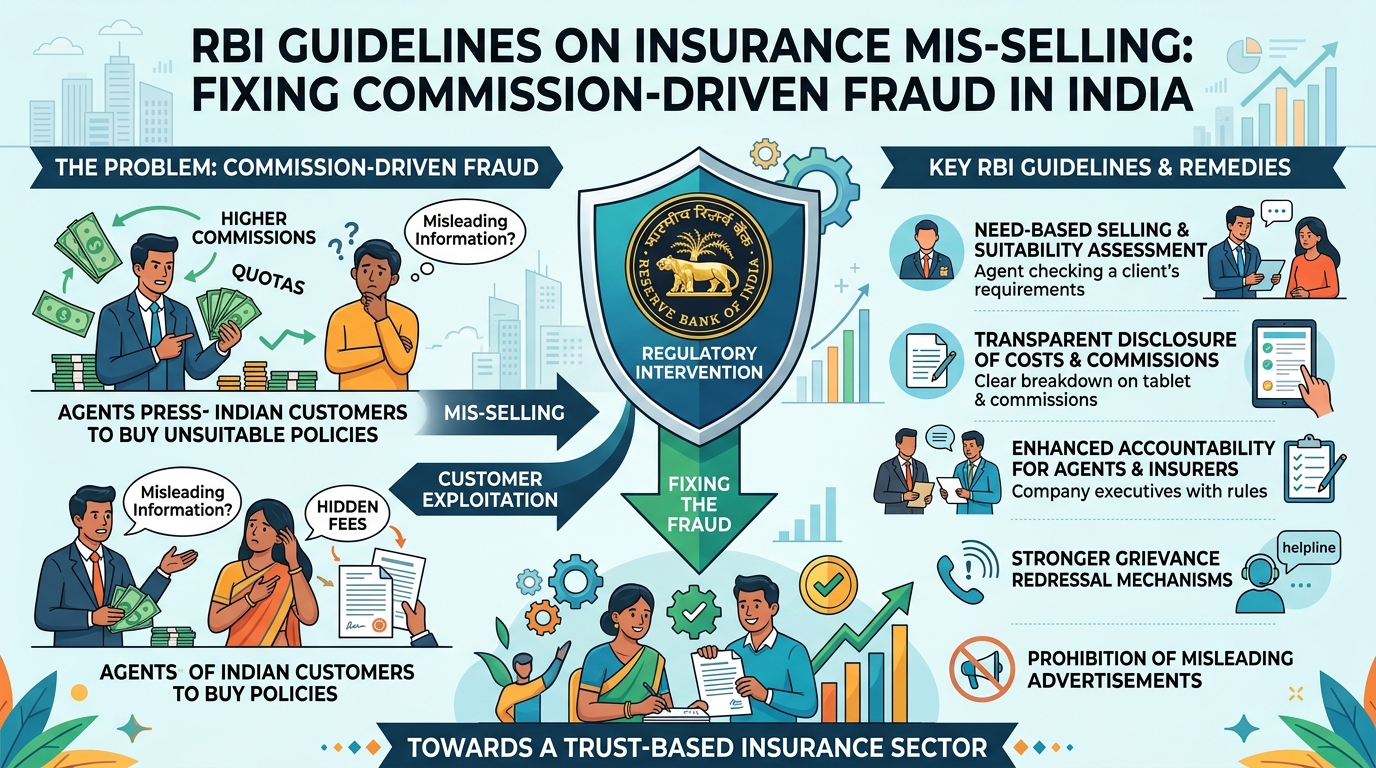

RBI Guidelines on Insurance Mis-selling: Fixing Commission-Driven Fraud in India

Table of Contents

The issue of insurance mis-selling shows that financial products cannot be treated like ordinary goods because they directly affect the security of families. The current system has created incentives that encourage quick sales instead of long-term customer welfare. A balanced approach that combines regulation, accountability, and awareness can create a fair system where both customers and companies benefit. The shift towards ethical practices will not only reduce mis-selling but also build a stronger and more inclusive financial system in the country.

Why in the News?

- The Reserve Bank of India is planning to release final guidelines on “Responsible Business Conduct” to protect customers from mis-selling by banks.

- These guidelines are expected to come into force from July 1, 2026.

- The focus is on improving how banks sell third-party financial products such as insurance.

- The aim is to make the process safer, more transparent, and fair for customers.

- At the same time, the Insurance Regulatory and Development Authority of India is also examining the issue of rising commissions paid by insurance companies.

- This issue is important because commissions are seen as the main reason behind mis-selling practices.

What are the Key Highlights?

RBI’s Responsible Business Conduct Guidelines

- RBI wants banks to follow ethical practices while selling financial products.

- Banks must ensure that customers understand the product clearly before buying it.

- The guidelines will focus on:

- Proper disclosure of product features, risks, and costs.

- Avoiding misleading sales tactics.

- Ensuring that products match the needs of customers.

Insurance Mis-selling

- Mis-selling means selling a product that is not suitable for the customer.

- It can also mean hiding important details or giving false information.

- In many cases, customers are forced or misled into buying expensive insurance policies.

- Example: An elderly woman was asked to withdraw her fixed deposits to buy a single-premium insurance policy.

Role of Commissions to curb the Insurance Mis-selling

- Insurance agents and bank staff earn commissions when they sell policies.

- These commissions can be very high, especially for new policies.

- According to IRDAI data:

- Total life insurance commissions reached ₹60,800 crore in FY25.

- Commissions grew faster than insurance premiums.

- High commissions create strong incentives to sell more policies, even if they are not suitable.

Rising Trends in Commission Structure

- First-year commissions increased by more than 20%.

- Single-premium policy commissions increased by nearly 37%.

- This shows that insurers are focusing on aggressive customer acquisition strategies.

IRDAI’s Proposed Reforms

- IRDAI is considering:

- Fixing commission rates directly.

- Introducing caps on commissions.

- Setting limits based on total management expenses.

- Earlier, IRDAI tried to control overall expenses instead of directly limiting commissions.

Alternative Suggestions by Industry Experts

- Experts believe direct caps may not solve the problem completely.

- They suggest:

- Making company boards responsible for deciding commissions.

- Introducing board-approved commission policies.

- Another important suggestion is to shift to a “trail-based commission model.”

Understanding Key Concepts

What is Insurance?

- Insurance is a financial product that provides protection against risks.

- It acts as a safety net for families in case of accidents, illness, or death.

What is Insurance Mis-selling

- Mis-selling happens when a product is sold unfairly.

- The customer is not given full or correct information.

- The product may not match the customer’s needs.

What is Commission?

- Commission is the payment given to agents for selling insurance policies.

- It is usually a percentage of the premium paid by the customer.

What is Front-loaded Commission?

- In this system, most commission is paid at the time of sale.

- Agents earn a large amount immediately after selling the policy.

- This encourages agents to focus only on selling, not on customer service.

What is Trail-based Commission?

- In this system, commission is paid over time.

- Agents receive payments as long as the policy continues.

- This ensures that agents stay connected with customers.

What is Expense of Management (EOM)?

- EOM includes all expenses of an insurance company.

- It includes commissions, administrative costs, and operational expenses.

What are the Significance?

Protection of Consumers

- These guidelines will protect customers from being cheated.

- Customers will receive clear and correct information before buying insurance.

Improvement in Trust

- When customers feel safe, their trust in the insurance sector increases.

- This helps in expanding insurance coverage in the country.

Better Financial Decisions

- Customers will be able to choose products based on their needs.

- This reduces financial losses and stress.

Strengthening Financial System

- Ethical practices improve the overall stability of the financial system.

- It reduces disputes and complaints.

Encouraging Long-term Relationships

- Trail-based commissions will encourage agents to maintain long-term relationships.

- Customers will receive continuous support and advice.

Better Product Design

- Insurance companies will focus on creating efficient and customer-friendly products.

- Products will be designed for long-term benefits, not quick sales.

Reduction in Exploitation of Vulnerable Groups

- Elderly people and less-informed customers are often targeted.

- New rules will reduce such exploitation.

What are the Challenges?

High Dependence on Commissions

- The insurance industry depends heavily on commissions to drive sales.

- Reducing commissions may affect sales growth in the short term.

Resistance from Industry

- Insurance companies and agents may oppose strict rules.

- They may argue that it will reduce their income.

Difficulty in Monitoring

- It is difficult to monitor every sale made by agents.

- Mis-selling may still happen in hidden ways.

Lack of Financial Awareness

- Many customers do not understand financial products.

- This makes them easy targets for mis-selling.

Conflict Between RBI and IRDAI

- RBI regulates banks, while IRDAI regulates insurance companies.

- Lack of coordination may reduce the effectiveness of reforms.

Front-loaded Incentive Culture

- The current system rewards quick sales.

- Changing this culture will take time.

Implementation Challenges

- Ensuring that all banks and agents follow new rules is difficult.

- There may be gaps in enforcement.

What is the Way Forward?

Shift to Trail-based Commission Model

- Commissions should be spread over the life of the policy.

- This will align the interests of agents with customers.

Strengthening Board Accountability

- Insurance company boards should be responsible for commission policies.

- This will ensure better governance and accountability.

Better Coordination Between Regulators

- RBI and IRDAI should work together closely.

- Joint efforts will improve regulation and enforcement.

Enhancing Financial Literacy

- Customers should be educated about financial products.

- Awareness programs should be increased across the country.

Use of Technology

- Digital tools can help track sales practices.

- Technology can identify unusual patterns and prevent fraud.

Strict Penalties for Mis-selling

- Strong action should be taken against wrong practices.

- This will discourage unethical behavior.

Transparent Disclosure Norms

- All charges and risks should be clearly explained.

- Customers should receive simple and easy-to-understand documents.

Customer-centric Approach

- The focus should be on customer needs, not sales targets.

- Products should match the financial situation of customers.

Conclusion

The issue of insurance mis-selling shows that financial products cannot be treated like ordinary goods because they directly affect the security of families. The current system has created incentives that encourage quick sales instead of long-term customer welfare. A balanced approach that combines regulation, accountability, and awareness can create a fair system where both customers and companies benefit. The shift towards ethical practices will not only reduce mis-selling but also build a stronger and more inclusive financial system in the country.

Relevant Articles:

ISRO Mission MITRA Boosts Gaganyaan Programme with High-Altitude Human Space Research

INS Aridhaman Boosts India Nuclear Triad Power and Maritime Strength

Read More:

Plastic Waste Management Rules 2026 Raise Concerns Over Weakened Compliance

NaMo Drone Didi Yojana Success: Karnataka Leads Women Drone Pilots

As RBI gears up to issue guidelines to curb mis-selling …